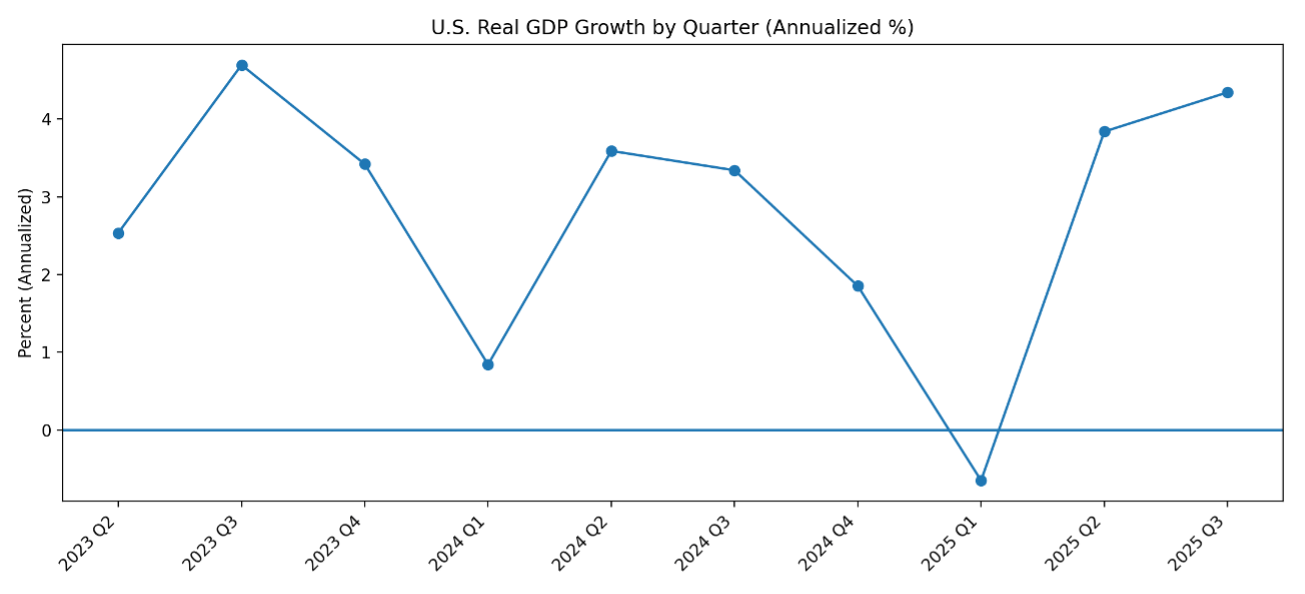

Stocks surged and Stock markets hit record highs in 2025 – All three indexes hit record highs in 2025 but closed the year slightly off their record highs. AI and robust economic growth fueled the rise in stock prices. The Dow Jones Industrial Average ended the year at 48,063.29, up 13% from 42,544.72 on December 31, 2024. The S&P 500 closed the year at 6,845.50, up 16.4% from 5,881.63 on December 31, 2024. The NASDAQ closed at 23,241.99, up 20.4% from 19,310.79 at the end of 2024. GDP surged in the third quarter of 2025 – The U.S. Gross Domestic Product (GDP), the broadest measure of goods and services in the economy, grew at a staggering 4.3% annualized rate in the third quarter of 2025. Earlier in the year, some economists had predicted that the economy was stalling and that a recession could be coming. The pickup in GDP has demonstrated that the economy has remained strong. This was one of the factors that propelled the stock markets this year.

The graph below shows the GDP rate over the past three years

U.S. Treasury Bond Yields – Treasury bond yields ended the year with short-term yields lower and long-term about the same as they were at the beginning of the year – The 10-year U.S. Treasury bond yield closed the year at 4.18%, down from 4.58% on December 31, 2024. The 30-year treasury yield ended the year at 4.84%, up from 4.78% on Dec. 31, 2024. We watch bond yields because mortgage rates often follow Treasury bond yields.

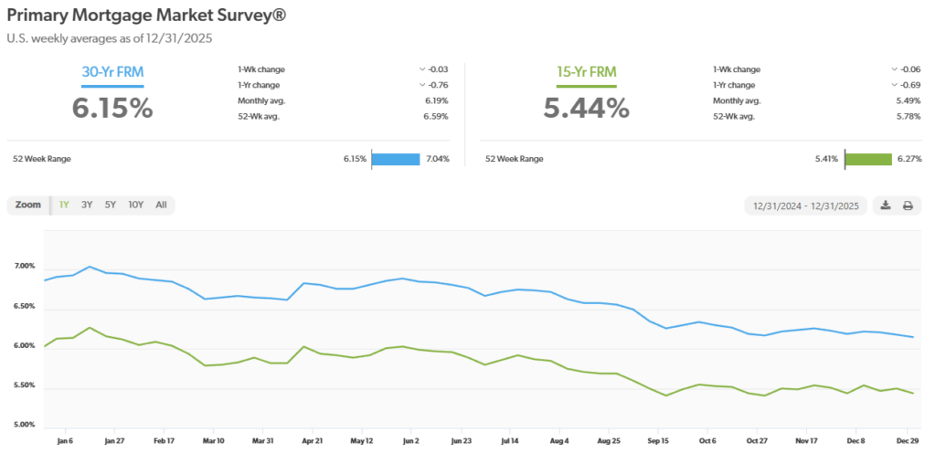

Mortgage rates dropped in 2025 – Experts expect them to drop further in 2026 –The Freddie Mac Primary Mortgage Survey reported that mortgage rates for the most popular loan products as of December 31, 2025, were as follows: The 30-year fixed mortgage rate was 6.15%, down from 6.85% on December 26, 2024. The 15-year fixed was 5.44%, down from 6% on December 26, 2024.

The graph below shows the trajectory of mortgage rates over the past year.

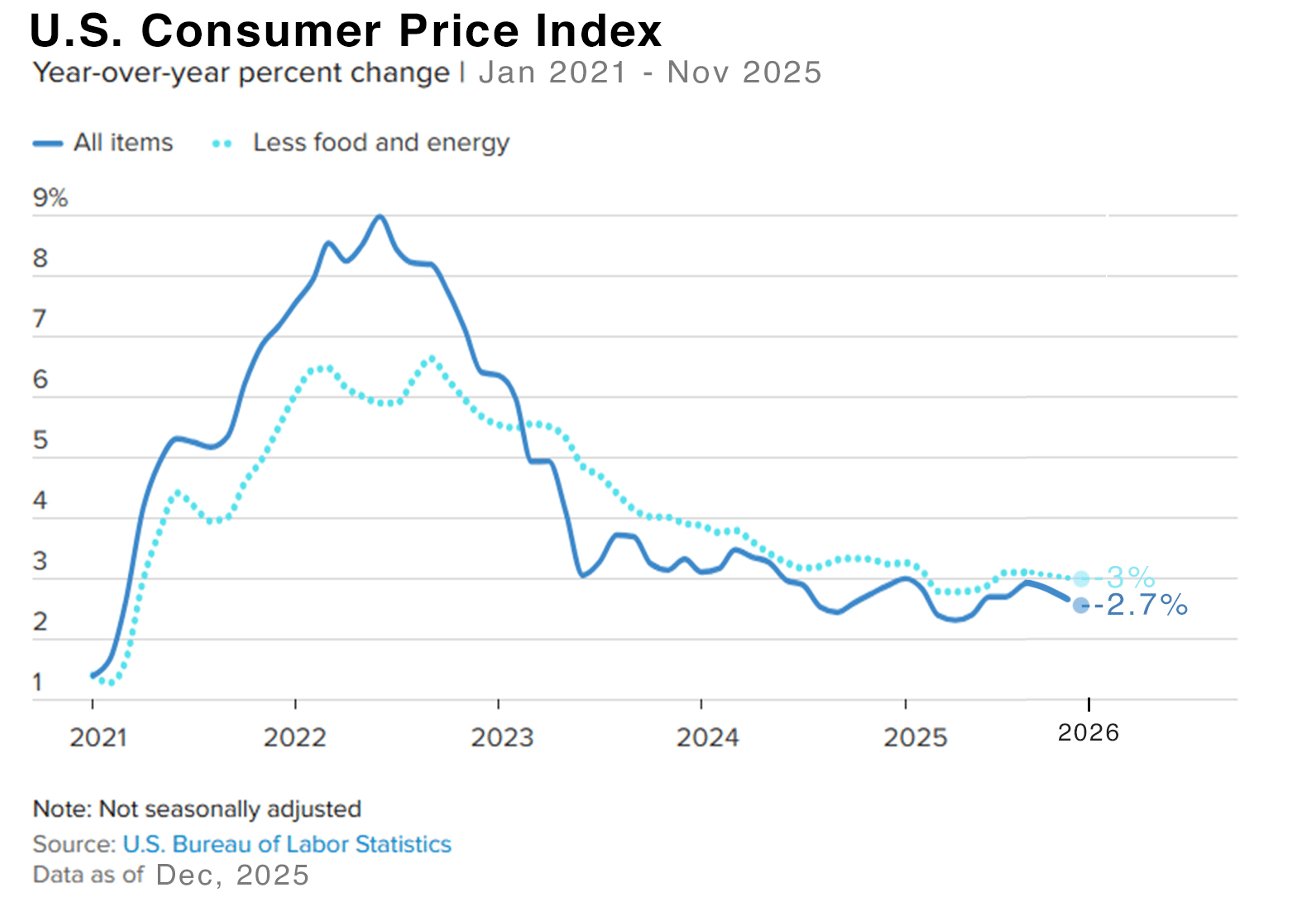

Inflation – We watch inflation because mortgage interest rates are tied to inflation. The higher the inflation rate, the higher the mortgage rates are. As inflation cools, mortgage rates drop. While we look at many different inflation reports, we have less data this year than we normally have because key indexes have not been released due to the government shutdown. One report, the Consumer Price Index (CPI) for November, was released. It showed that consumer prices rose 2.7% from one year ago in November. While still far from the Fed’s 2% annual target, it was much lower than the 3.1% that economists polled expected. The CPI rate peaked at 9.1% in June 2022 and worked its way down to 2.3% in April. Unfortunately, the CPI rate began to increase from there and peaked at 3% in September, which economists attribute to tariff costs being passed on to consumers, before dropping to 2.7% in November. The core CPI rate, which excludes volatile food and energy prices, rose 2.6% from one year ago, also below economists’ expectations. This gave hope to investors that inflation may be cooling enough for the Fed to continue to lower rates. The Fed’s favorite measure of inflation is the Personal Consumption Expenditure Index (PCE).Unfortunately, due to the shutdown, the October and November numbers are still being tabulated and are scheduled for release with the December figures at the end of January. For September, it showed that headline PCE rose 0.3% in September from August. That was in line with economists’ expectations. On an annual basis, PCE rose 2.7% from one year earlier, below the 2.8% expected. Core PCE, which does not include food and energy prices because those tend to be more volatile, increased 0.2% month-over-month in September. On an annual basis, it was up 2.8% from one year earlier. That was below the 2.9% economists expected.

November home sales – The California Association of Realtors and the National Association of Realtors release home sales data on the third week of each month for the previous month. Here is the November 2025 home sales recap. You can run a report on your city or zip code with the same data at RodeoRe.com

U.S. existing-home sales – November 2025 – The National Association of Realtorsreported that existing-home sales totaled 4.13 million units on a seasonally adjusted annualized rate in November, up 0.5% from the number of homes sold in October and down 1% from the number of homes sold last November. The median price paid for a home sold in the U.S. in November was $409,200, down from $415,200 in October, but up 1.2% from $404,400 one year ago. There was a 4.2-month supply of homes for sale in November, up from a 3.8-month supply last November. First-time buyers accounted for 30% of all sales, up from 30% last month. Investors and second-home purchases accounted for 18% of all sales, down from 15% in August. All cashpurchases accounted for 27% of all sales, up from 30% last month. Foreclosures and short sales accounted for 2% of all sales.

California existing-home sales – The California Association of Realtors reported that existing-home sales totaled 287,940 on an annualized basis in November, up 1.9% from 285,590 in October. Year-over-year sales were up 2.6% from a revised 280,530 annualized home sales last November. The statewide median price paid for a home was $852,680 in November, down 3.9% from 886,960 in October. Year-over-year, the median price was almost unchanged from $852,880 last November. The unsold inventory index showed that there was a 3.1-month supply of homes for sale in October. These numbers are a little deceiving. Prices have dropped more than the median price indicates. The median price is the mid-point of all homes sold. Basically, it’s the point where one half of the homes sold for more and one half of the homes sold for less. Usually, the median price is a good indicator of prices across the board. There are times when conditions impact that. This is one of those times. With stock market values at all-time highs, which they were in October, people who invested in the stock market are flusher than people who are not. Additionally, many of the factors that impact people’s ability and desire to buy a home affect people more in the lower income range than they affect people in higher income ranges. That’s happening now. Sales are down in all price ranges compared to any time prior to interest rates rising in mid-2022, but sales in the lower price ranges as a percentage of all sales are fewer than we would normally see, as those people are more impacted by inflation, don’t have stocks, etc.

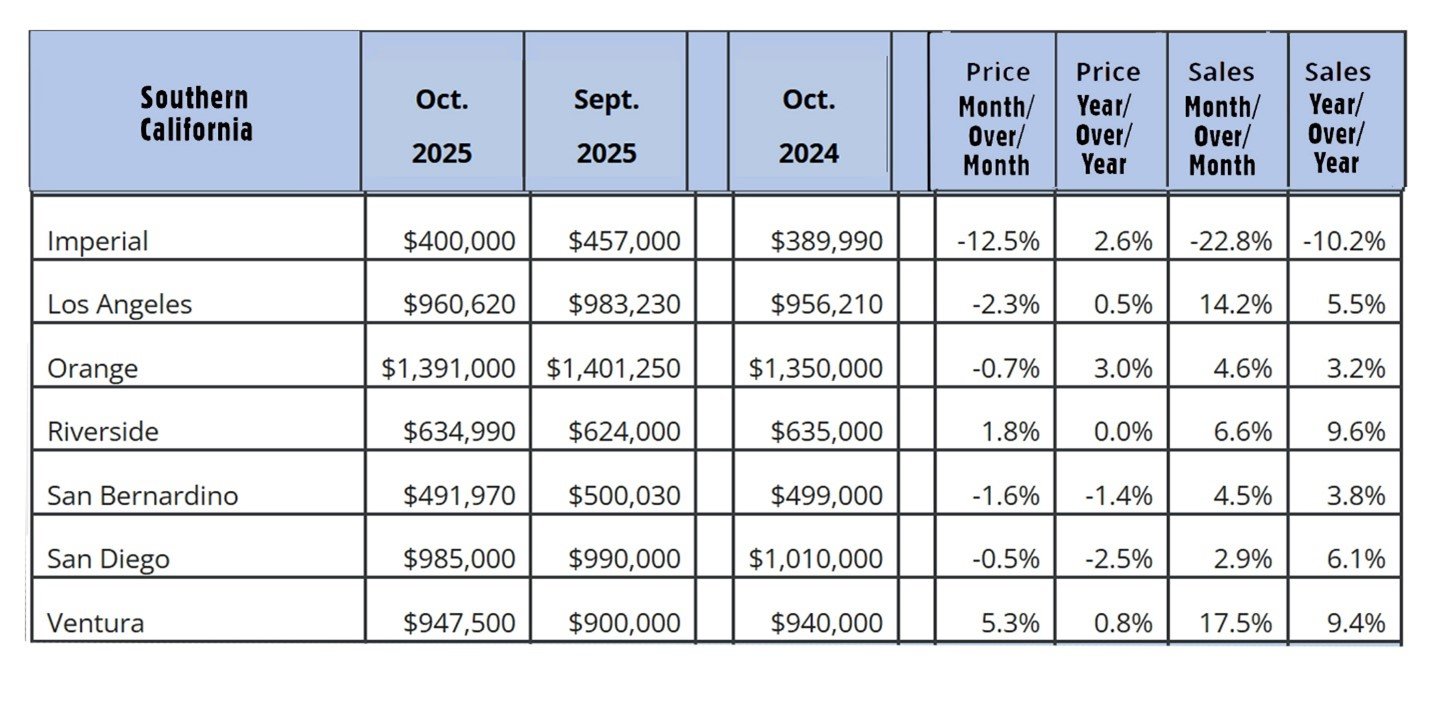

The graph below shows CAR sales data by county for Southern California.